KTL Expands Food Safety Resources

KTL is pleased to welcome the following new food safety resources to our team!

Samantha Humphrey, Consultant

Sam has 10 years of experience working in the food and beverage industry. She has specialized expertise in food safety training; regulatory compliance, particularly the FDA Produce Safety Rule; GMPs and GAPs; SOP development and implementation; GFSI certification; supply chain management; environmental monitoring; and food microbiology. Sam is a PCQI and Produce Safety Rule Lead Trainer, Certified ATD Master Trainer, Certified Professional – Food Safety (CP-FS), and Juice and Seafood HACCP certified. She is based in Raleigh, NC. Read her full bio…

shumphrey@goktl.com | 919.818.7858

Rachel Thomashow, Consultant

Rachel is an FSQA professional with nearly five years of experience working in the food industry. Her background includes compliance with GFSI requirements and GMPs, supplier documentation, research and development, and product quality verification. She further has experience working in a laboratory and performing analytical tests on food products. Rachel is a PCQI and HACCP certified. She is based in Chicago, IL. Read her full bio…

rthomashow@goktl.com | 847.769.5760

Comments: No Comments

Climate-Related Disclosures: SEC Final Rule

Agencies across the globe have implemented various voluntary and mandatory sustainability and carbon disclosure reporting requirements, ranging from the International Financial Reporting Standards (IFRS) Sustainability Disclosure Standards, to the EU Corporate Sustainability Reporting Directive, to the State of California’s climate disclosure legislation. Even the International Organization for Standardization (ISO) recently issued an amendment to ensure climate change impacts are considered by all organizations in their management system design and implementation.

On March 6, 2024, the U.S. Securities and Exchange Commission (SEC) followed suit, approving its much-anticipated final rule: The Enhancement and Standardization of Climate-Related Disclosures for Investors (Climate-Related Disclosure Rule). Initially proposed in March 2022, the SEC’s final rule requires publicly listed companies to report on greenhouse gas (GHG) emissions; climate-related risks; and other relevant environmental, sustainability, and governance (ESG) information. According to the SEC, the final rules are a continuation of the SEC’s efforts to respond to investor needs for more consistent, comparable, and reliable information about the financial effects of climate-related risks on a registrant’s business.

Overview of Requirements

The SEC’s recent action represents a significant milestone in the U.S., as it integrates climate-related risks and opportunities into business practices and investment decisions. Fundamentally, the final rule requires companies to:

- Identify any material climate-related risks, assess their impacts on financial performance and business strategy, and outline activities to mitigate or adapt to such risks.

- Disclose how they manage the oversight and governance of identified climate-related risk (i.e., the role of management and the Board of Directors).

- Provide information on any climate-related targets or goals that are material to the registrant’s business or financial condition.

- Provide comprehensive disclosure and attestation reporting on Scope 1 (i.e., direct) GHG emissions and Scope 2 (i.e., indirect) GHG emissions (large accelerated filers (LAF) and accelerated filers (AFs)).

- Disclose financial impacts of severe weather events and other natural conditions.

The final rule modifies the March 2022 proposed rule in several ways, most notably by removing the requirement for Scope 3 GHG emission disclosures and providing more time to implement disclosures and related assurance requirements. The SEC Fact Sheet provides a more comprehensive overview of all requirements included in the final rule.

The SEC Fact Sheet provides a more comprehensive overview of all requirements included in the final rule.

Timeline for Compliance

The final rule becomes effective 60 days after publication in the Federal Register. The requirements will be phased in for all registrants with the compliance date dependent upon the status of the registrant as an LAF, AF, or non-accelerated filer (NAF); smaller reporting company (SRC); or emerging growth company (EGC) and the content of the disclosure. Initial deadlines for Scope 1 and 2 GHG disclosures for LAFs begin as early as FY 2026. Refer to the SEC Fact Sheet for a breakdown on all deadlines.

What to Do

If it isn’t happening already, facilities need to start gathering emissions data, develop and implement a system to track GHG emissions, and create an action plan for climate disclosure. Even non-publicly traded companies can benefit from adhering to the general requirements of the new regulations, as publicly traded customers may require climate-related information. This presents an opportunity to demonstrate a commitment to ESG and improve brand reputation; an energy consumption analysis can also lead to improved efficiencies and cost savings.

For many, the SEC’s final rules have the potential to significantly expand requirements beyond what the company is already doing. The transition timeline is designed to allow companies the time needed to:

- Ensure the company has a robust management system in place to provide a solid framework for conducting the required risk assessments, managing new reporting requirements, and organizing required documentation. Note that ISO has taken recent steps to build climate change considerations into all its management system standards.

- Understand current disclosure reporting capabilities, data requirements, processes, and controls, then analyze what climate-related data has already been gathered and what additional information is needed to comply with the final rule.

- Establish or refine corporate governance and define clear roles, responsibilities, and charters for management oversight.

- Develop an action plan for implementation and integrate it with any other existing climate-related initiatives.

As organizations prepare to meet SEC disclosure requirements, KTL can help ensure they have the systems and processes in place to comply and to realize sustainable business value, including:

- Developing and implementing management systems that incorporate climate change considerations, including identifying environmental aspects and impacts, risks, and opportunities.

- Conducting energy audits and analyzing enterprise-wide energy consumption, trends, and opportunities for improvement.

- Calculating and tracking Scope 1, 2, and 3 GHG emissions.

- Identifying and planning for GHG emission reduction targets, renewable energy projects, and other opportunities to improve the organization’s carbon footprint.

- Developing information management tools to manage and track data and trend goals and objectives related to climate change.

FAQs on ISO’s New Climate Change Amendments

Effective February 23, 2024, the International Organization for Standardization (ISO) is integrating climate change considerations into all management system standards through its Climate Change Amendments. These Amendments ensure climate change impacts are considered by all organizations in their management system design and implementation.

ISO’s recent action supports the London Declaration on Climate Change of September 2021, which establishes ISO’s commitment to combatting climate change through its standards and publications. The aim of the recent Amendments is to make climate change an integral part of management systems design and implementation to help guide organizational strategy and policy.

What are the changes?

The Climate Change Amendments explicitly require climate change considerations in all existing and future ISO management systems standards, as incorporated into the Harmonized Structure (Appendix 2 of the Annex SL in the ISO/IEC Directives Part 1 Consolidated ISO Supplement). More specifically, the Amendments add the following two new statements to Annex SL for organizations to consider the effects of climate change on the management system’s ability to achieve its intended results:

- Clause 4.1: The organization shall determine whether climate change is a relevant issue, as it relates to understanding the organization and its context.

- Clause 4.2: NOTE: Relevant interested parties can have requirements related to climate change, pertaining to understanding the needs and expectations of interested parties.

The broad scope of these Amendments (i.e., impacting all standards) reflects ISO’s commitment to integrating climate considerations across diverse operational areas (e.g., environment, quality, safety, food safety, security, business continuity, etc.).

What do these changes require?

The original intent and requirements of Clauses 4.1 and 4.2 remain unchanged; however, the Amendments now require organizations to consider the relevance of climate change risks and impacts on the management system(s).

Potential climate change issues will likely differ for the various standards. The Amendments ensure these various risks are considered for each standard and, if actions are required, allow the organization to effectively plan for them in the management system.

What do certified organizations need to do?

Organizations that are certified—or are planning for certification—need to make sure they consider climate change aspects and risks in the development, maintenance, and effectiveness of their management system(s).

The Amendments specifically require these organizations to evaluate and determine whether climate change is a relevant issue within their management system(s). If the answer is yes, the organization then must consider climate change in a risk evaluation within the scope of their management systems. Where relevant, organizations are further encouraged to integrate climate change into their strategic objectives and risk mitigation efforts. The Amendments do not require organizations to do anything about climate change beyond considering the impacts on the management system’s ability to achieve its intended results.

What is the timeline?

The Amendments are effective as of the date of publication. There is no transition for implementation.

Certification bodies and auditors will cover the Amendments in audit activities when assessing this section of a management system. The audit will ensure climate change is considered and, if determined to be a relevant issue, included in company objectives and risk mitigation efforts. If climate change is deemed not relevant, the audit will assess the organization’s process for making this determination.

Will new certifications be issued?

Because the changes are considered a clarification, ISO issued them in the form of an amendment. New standards will not be republished until new versions are released; therefore, the publication year of each ISO standard will not change, and no new certifications will be issued.

What are the benefits of these changes?

The Climate Change Amendments underscore the importance of understanding and addressing the impacts of climate change. By publishing the Amendments in Annex SL, ISO is leveraging the widespread adoption of all ISO management system standards across operational areas to integrate environmental stewardship into organizational practices, promote sustainability, and drive climate change action on a global scale.

For certified organizations, the Amendments are intended to enhance organizational resilience and adaptability to climate-related risks. Considering climate change in this way can significantly contribute to business sustainability and long-term success by:

- Ensuring regulatory compliance (e.g., emission limits, sustainability reporting, etc.).

- Creating positive brand reputation as a sustainable company and associated customer loyalty.

- Managing risks and opportunities associated with supply chain disruptions, energy efficiency initiatives, employee health and safety, natural disasters, etc.

- Engaging employees and attracting new talent who prioritizes sustainability.

- Providing access to markets and investors that have sustainability requirements.

Comments: No Comments

Risk Management Program (RMP) Amendments Finalized

On February 27, 2024, the U.S. Environmental Protection Agency (EPA) signed the much-anticipated final amendments to the Risk Management Program (RMP) Rule—known as the Safer Communities by Chemical Accident Prevention (SCCAP) Amendments—to further protect high-risk communities from chemical accidents. According to the EPA press release, the SCCAP Amendments include EPA’s most protective safety provisions for chemical facilities in history, requiring stronger measures for prevention, preparedness, and public transparency.

RMP Primer: A Sordid History

Just what the RMP Rule entails has been the subject of debate since EPA first proposed the RMP Amendments in 2017. Rules related to RMP requirements have been published, petitioned, delayed, vacated, reissued, and reconsidered. In November 2019, EPA Administrator Andrew Wheeler signed the RMP Reconsideration Rule, rescinding or modifying many of the measures of the 2017 Amendments. In August 2022, EPA proposed, once again, to strengthen the RMP regulations with the proposed SCCAP Amendments, which were finalized on February 27, 2024.

RMP regulates approximately 11,740 facilities in the U.S. that use extremely hazardous substances, including agricultural supply distributors, waste/wastewater treatment and end-of-life processing facilities, chemical manufacturers and distributors, food and beverage manufacturers, chemical warehouses, oil refineries, and other chemical facilities.

Fundamentally, the RMP Rule has always required facilities storing specific chemicals above certain threshold amounts to develop Risk Management Plans to prevent and mitigate accidents that could release those chemicals into the environment and cause injury or death, damage property and the environment, or require communities to evacuate or shelter-in-place. The Risk Management Plan is intended to:

- Identify potential impacts of a chemical accident on human health and the environment.

- Outline steps the facility is taking to prevent an accident.

- Detail emergency response procedures in the event of an accident.

The Rule also contains more rigorous requirements for a subgroup of facilities that are more prone to accidents and pose the greatest risk to the community.

Amendments

The SCCAP Amendments include several new requirements that require RMP-regulated chemical facilities to better consider surrounding communities, including the impacts of climate change, environmental justice concerns, employee participation, and enhanced community notification.

Historically underserved and overburdened populations disproportionately live in closest proximity to RMP facilities. In fact, according to EPA, approximately 131 million people live within three miles of RMP facilities and 44 million of these individuals earn less than or equal to twice the poverty level. The Amendments focus on increasing transparency and access to RMP information for communities living and working around the surrounding areas, as well as supporting President Biden’s Justice40 Initiative to protect disadvantaged communities.

In addition to the major amendments outlined in the table below, EPA is working to increase transparency by making RMP information more accessible through a public data tool, which will allow people to access information for RMP facilities in nearby communities.

| Area | Amendment |

| Safer Technology Alternatives Analysis (STAA) | Requires a STAA and, in some cases, implementation of reliable safeguards (e.g., inherently safer technologies and designs (IST/ISD), passive measures, active and procedural measures) for certain facilities in industry sectors with high accident rates (i.e., Program 3 NAICS 324 and 325 processes). |

| Employee Engagement | Advances employee participation, training, and decision-making in facility accident prevention, including: – Encouraging employee participation in resolving findings from process hazard analyses, compliance audits, and incident investigations. – Allowing for partial or complete process shutdown (i.e., stop work procedures) in the event of a potential catastrophic release. – Implementing a process for employees to anonymously report unaddressed hazards. – Requiring training on employee participation plans. |

| Root Cause Analysis Third-party Compliance Audits | Requires third-party compliance audits and root cause analysis incident investigations when facilities have had a prior RMP-reportable accident. |

| Emergency Response | Enhances facility planning and preparedness efforts to strengthen emergency response by: – Requiring facilities to develop procedures to inform the public about accidental releases. – Ensuring chemical release information is shared with local emergency planning commissions (LEPCs) in a timely manner. – Partnering with LEPCs to establish a community notification system to warn of impending releases. – Requiring 10-year field exercises for emergency response, as well as related mandatory scope and reporting requirements. |

| Natural Hazards | Requires facilities to evaluate risks of natural hazards and climate change and provide a backup power source for release monitoring equipment. |

| Information Sharing | Increases transparency by requiring facilities to provide chemical hazard information in the two most common languages spoken by individuals living, working, or spending significant time within six miles of the facility. |

| Facility Siting | Requires facility siting to be addressed in hazard reviews and explicitly defines facility siting requirements for Program 2 hazard reviews and Program 3 process hazard analyses. |

The Rule also includes several minor regulatory edits to clarify requirements related to recognized and generally accepted good engineering practices (RAGAGEP), hot work permits, retail facility exemptions, amongst others. Any new provisions that are not adopted require a written justification as part of the Risk Management Plan.

Timeline

Most provisions, including STAA, incident investigation root cause analysis, third-party compliance audit, employee participation, emergency response public notification, exercise evaluation reports, and information availability provisions have a deadline of three years after the effective date.

Facilities have until March 15, 2027 to conduct revised emergency response field exercises (or within 10 years of the date of an emergency response field exercise conducted between March 15, 2017 and August 31, 2022).

All updates to and resubmission of Risk Management Plans with revised data elements are due four years after the Rule’s effective date.

Next Steps

For RMP facilities, it is important to:

- Understand the hazards posed by chemicals at the facility and assess the impacts of a potential release.

- Review the Amendments to determine what updates need to be made to the facility’s Risk Management Plan and when.

- Prioritize your compliance risks and develop strategies to minimize them to the extent possible, including:

- Outlining steps to improve performance and safe operations.

- Defining organizational roles and responsibilities.

- Designing and maintaining a safe facility to prevent accidental releases.

- Minimize the consequences of accidental releases that do occur.

- Coordinate with local emergency responders to plan and conduct required tabletop exercises to ensure your plans work in practice.

- Streamline compliance methods and improve operational efficiencies by implementing IT solutions and compliance management systems that coordinate, organize, control, analyze, and visualize information.

KTL has experience working with a broad cross-section of industries impacted by RMP, particularly chemical companies. We have created RMP and General Duty Clause audit protocols, conducted audits and investigation/improvement programs following significant release events. In addition, our team provides Tier II and TRI reporting, writes plans for OSHA and Emergency Response, routinely works with LEPCs to coordinate emergency response efforts and exercises to keep communities informed and safe.

Comments: No Comments

What Is an Energy Audit–And Why You Should Do One

Want to reach your sustainability goals, improve your energy efficiency, and save money? An energy audit can help you better understand your energy usage and issues—and identify opportunities to create energy efficiencies, reduce your carbon footprint, and positively impact your stakeholders.

What Is an Energy Audit?

An energy audit is a key part of energy management. Energy management involves monitoring and controlling energy consumption across an organization to save energy, save money, and protect people and the environment. Energy management should be part of any organization’s overall strategy. An energy audit helps determine energy usage and opportunities for efficiency projects at your facility, building, or process. The overarching goal of an energy audit is ultimately to reduce energy consumption and improve efficiency without impacting work processes or products.

Types of Energy Audits

An energy audit can take a range of forms depending on how detailed and extensive it needs to be:

- Preliminary Analysis: Review bill, conduct energy usage trending.

- Treasure Hunt: Conduct a group exercise walking around identifying obvious wastes.

- General Audit: Analyze specific systems, conduct detailed inspection.

- Comprehensive Audit: In addition to the areas covered above, may include longer term monitoring and mechanical/electrical/civil engineering reviews.

- Ongoing Audit: Long-term monitoring of efficiency systems, scheduling retro-commissioning.

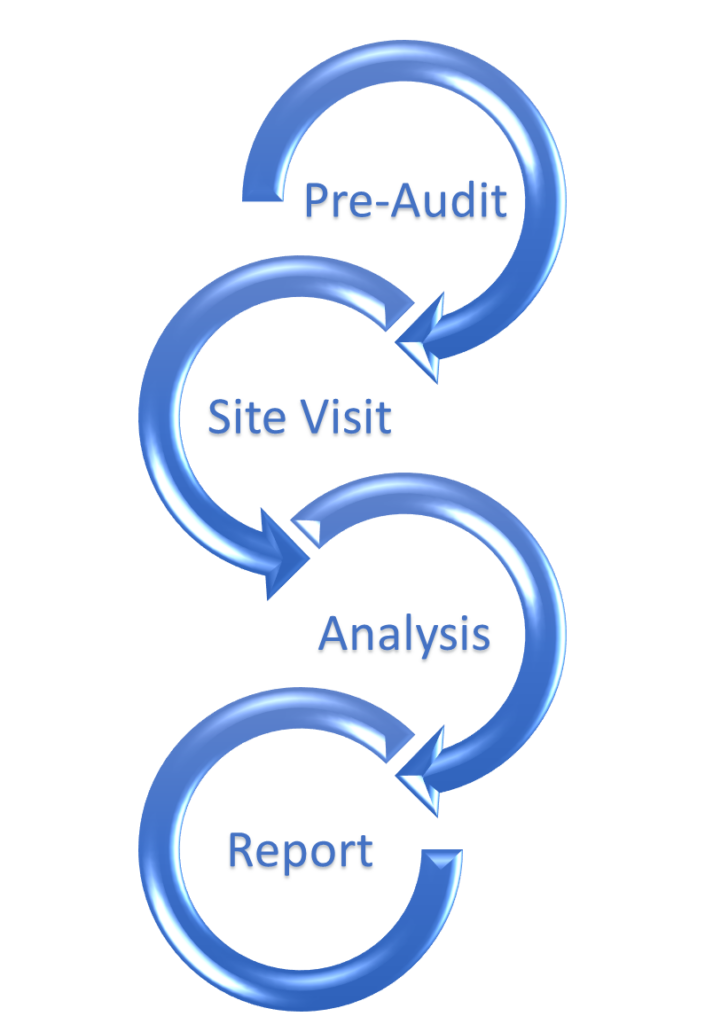

General Energy Audit Process

In general, the energy audit process comprises several steps and activities that culminate in final recommendations to improve energy performance and efficiency.

The pre-audit is a desktop review that helps to identify energy consumption patterns, including the energy “hogs” and peak usage trends (i.e., the hours of the day during which demand for electricity is the highest). It consists of the following activities:

- Review utility bill for demand charges, power usage, load factor.

- Demand charges are fees applied based on the highest amount of power drawn during any interval during the billing period. Demand charges can comprise a significant proportion of commercial customers’ bills.

- Load factor is a measure of the utilization rate or efficiency of electrical energy usage. It is an indicator of how efficiently energy is being utilized.

- Review equipment repair and occupant complaint logs.

- Review past audit results.

- Discuss with management internal goals, financial criteria, upgrades, and future plans.

The site visit allows the auditor to observe facility operations and assess how systems are operating in practice. It comprises activities such as the following:

- Conducting interviews with operators, key decision-makers, and other plant staff.

- Collecting data, including facility data, nameplate data, forms, and logs.

- Performing a site walkthrough/tour to review:

- Site development.

- Building envelope.

- BTUs of boiler/HVAC, compressors, refrigeration, large equipment, etc.

- Building exterior (e.g., roof plan, outdoor lighting, exterior equipment).

- Taking measurements (i.e., combustion, lighting, temperature, ultrasonic).

After collecting the pre-audit documentation and site visit observations, the auditor is able to then perform a detailed analysis of energy performance. This analysis involves calculating the following:

- Energy usage, including baseload and peak energy, adjusted for weather, occupancy, and production.

- Energy costs, including accurate application of rates, time of use applications, seasonal applications, utility bill ratchet.

- Energy efficiency measures (EEMs), including material and installation, disposal, engineering design, permits and fees, and rebates and incentives.

The final report provides an action plan highlighting short-term (i.e., low-hanging fruit) opportunities, long-term budgeted improvements, and company goals. It should also reference site management, potential future problems, and testing programs that can all impact energy programs and operations.

Impacting People, Planet, and Profit

Energy audits directly impact the three Ps of the triple bottom line:

People. The United Nations has identified climate change as the number one threat to human societies. Brown energy releases can substantially impact air quality and have significant negative impacts on human health. Creating energy efficiencies and reducing the use of non-renewable energy is key to mitigating this threat. Beyond the human health threat, improved EEMs can improve employee satisfaction and, subsequently, create a corporate culture shift that embraces sustainability. For example, optimized lighting, ventilation controls, and incentives for driving electric vehicles may lead to healthier and happier employees and improved retention.

Planet. In its simplest terms, reducing energy usage helps reduce carbon footprint and mitigate the impacts of global warming. For example:

- Fossil fuels are a finite resource. Reliance on them leads to the destruction of protected ecosystems and habitat. Lower energy demand decreases the need for power generation and the use of fossil fuels.

- Energy audits identify ways to reduce energy use. This, in turn, reduces air emissions and global pollution levels. The equation is simple: the less energy you use, the fewer carbon emissions you produce.

- Beyond energy efficiencies, energy audits also identify waste. Eliminating these waste streams prevents unnecessary landfill use and contributes to environmental sustainability.

Profit. The Carbon Trust estimates that most businesses can cut their energy costs by at least 10% (often by 20%) with simple actions that offer a quick return on investment. Operating more efficiently reduces energy consumption, which equates to significant savings on utility bills. This is particularly important as energy costs reach all-time highs. In addition, organizations that consume significant amounts of energy are at greater risk of being impacted by energy price increases or supply shortages. When an organization can reduce its demand for energy, it also reduces the risks associated with an energy shortage. Having greater control over energy consumption creates resiliency against energy price fluctuations.

Return on Investment

Once you have a comprehensive understanding of how energy is being consumed, it becomes possible to identify inefficiencies and opportunities for improvement, whether related to behavior (e.g., asking employees to turn off lights every night), technology (e.g., implementing integrated building management systems), or process (e.g., increasing operations during off-peak hours).

Energy audits may identify the following opportunities to reduce costs:

- Reducing operational inefficiencies, including continual running of motors, unoccupied spaces (light sensors), compressed air leaks, and others.

- Implementing EEMs, such as monitoring systems for malfunctions, insulating hot/cold water piping, implementing efficient lighting, and ensuring heat recovery.

- Optimizing building systems, including ventilation systems, lighting control systems, insulation, efficient windows, green roofs, etc.

- Identifying financial incentives, rebates, and demand response programs.

Energy Audit Best Practices

To get the most out of an energy audit, it takes time, data, budget, and buy-in. The following can help ensure your audit is successful and provides return on investment:

- Start small, plan ahead. Select the right type of audit based on the resources (i.e., time, financial, personnel) you have available. You can scale up your efforts over time.

- Set clear objectives. Identify what your organization wants to get out of the audit. Consider the 3 Ps—people, planet, and profit—and be open-minded. It may be about energy savings and cost reduction, but it also may be about meeting sustainability goals, creating a culture change, or retaining and attracting employees.

- Gather data. Review utility bills. Trend energy consumption. Assess building specifications.

- Enlist audit expertise. Engage the right auditors with the right qualifications. A Certified Energy Manager (CEM) and someone with an engineering background can add a depth of expertise to help identify concerns and opportunities beyond the “low-hanging fruit”.

- Conduct routine inspections and assessments. Update your maintenance program to include steam trap surveys, compressed air leak inspections, duct cleaning, and other routine inspections. These routine inspections allow for early detection of costly issues, and predictive maintenance can help reduce downtime and expand equipment life.

- Conduct routine measurement and verification. Just because you have implemented a system, process, or equipment does not mean that it is functioning as intended. Assess your EEMs regularly to ensure they are achieving the desired results.

- Engage your stakeholders. Include management staff, employees, and other decision-makers in your efforts. Engaging these stakeholders in creating solutions can help create buy-in and a culture change that makes energy efficiency and sustainability a way of doing business.

Comments: No Comments

EHS: 2024 Trends on Tap

According to a December 2023 press release, the Environmental Protection Agency (EPA) moved further and faster than ever before to deliver on its mission and protect human health and the environment in 2023. These actions—in addition to other trends in business efficiency, employee safety, and sustainability—have given rise to several new (and some ongoing) challenges and opportunities in environment, health, and safety (EHS). As a new year begins, it is important that companies understand their obligations, assess potential impacts, and prioritize efforts to ensure ongoing compliance and business performance.

Here are some of the top EHS trends KTL is keeping watch on in 2024—and some guidance to help you as you set your EHS strategy for the new year.

New OSHA Reporting Requirements

The Occupational Safety and Health Administration (OSHA) is focused on increasing transparency regarding workplace injuries with its new reporting requirements, which are effective as of January 1, 2024. The Administration is requiring organizations with more than 100 employees in certain high-risk industries to electronically submit information from OSHA Forms 300 and 301 to OSHA annually. In addition, certain high-hazard industries are now required to submit case-specific information. The data is intended to allow employers, employees, customers, the public, and other stakeholders to make more informed decisions about workplace health and safety. The deadline to submit information via the Injury Tracking Application is March 2, 2024.

Guidance: Maintaining robust occupational health and safety and incident records becomes even more important with these enhanced reporting requirements. Information technology (IT) tools, such as KTL’s OSHA 300 PowerApp with its comprehensive intake form tailored to OSHA 300 and OSHA 300A requirements, make it easier to collect, search, and analyze data—and maintain OSHA compliance. Using a digital format helps ensure no crucial data points are missed and makes it easy to filter, search, and analyze records and data to offer deeper insights into safety performance.

Climate Change and Environmental, Social, and Governance (ESG) Standards

In March 2022, the U.S. Securities and Exchange Commission (SEC) issued a proposed ESG Disclosures Rule that would require companies to 1) disclose how they are dealing with oversight and governance of climate-related risks; 2) identify any material climate-related risks and articulate their impacts on financial performance; and 3) provide comprehensive reporting of Scope 1, 2, and 3 greenhouse gas (GHG) emissions.

Leading the way, California passed its Climate Corporate Data Accountability Act (SB 253) and Climate-Related Financial Risk Act (SB 261) in 2023 to address the physical, human, and financial risks associated with climate change by requiring companies publicly disclose GHG emissions and climate change threats. Thousands of organizations that do business in California will now have to provide carbon emissions data by 2026—and companies across the country need to be prepared to follow suit.

Guidance: If it isn’t happening already, facilities need to start gathering emissions data, develop and implement a system to track GHG emissions, and create an action plan for climate disclosure. Accurate carbon accounting and energy management will allow companies to gain a deeper understanding of their emissions profiles and implement changes to improve energy efficiency and sustainability. If managed appropriately, these new disclosure requirements can provide a significant opportunity for companies to demonstrate a commitment to corporate social responsibility and improve brand reputation.

EPA Regulatory Enforcement

According to EPA, enforcement has been revitalized. We saw this trend pick up in 2023 with significant investments being made to enforce compliance with the nation’s environmental laws, including $213 million for civil enforcement efforts, $148 million for compliance monitoring efforts, and $69 million for criminal enforcement efforts. The past year has brought increases in onsite inspections, new criminal investigations, civil settlements, and cleanup enforcement. In 2024, EPA intends to continue its enforcement path, holding environmental violators and responsible parties accountable.

Guidance: Facility audits and assessments offer a systematic, objective tool to assess compliance across the workplace and to identify any opportunities for improvement before they become findings in an EPA inspection. These audits can also present an opportunity for organizational learning and development, particularly related to non-conformances. Conduct a gap assessment to evaluate whether processes and systems are functioning as intended, and then implement corrective and preventive actions to ensure compliance, particularly at the time of inspection. Look at the big picture and consider changes in production and business operations that may also change compliance requirements.

Per- and Polyfluoroalkyl Substances (PFAS)

EPA continues to make significant contributions in research and regulations, according to the PFAS Strategic Roadmap, to confront the human health and environmental risks of PFAS. In October 2023, the Agency finalized two new rules to improve reporting on PFAS. This January, EPA finalized a rule to prevent inactive PFAS from reentering commerce and added seven additional PFAS to Toxics Release Inventory (TRI) reporting. The Food and Drug Administration (FDA) is further working to understand and limit PFAS in food and food packaging.

Guidance: It is important for facilities to have a good understanding of PFAS and PFAS-containing chemicals used onsite, as reporting requirements now apply regardless of the quantity used. Implementing a chemical inventory management system that documents and manages PFAS data can make reporting more efficient and help ensure the facility meets these new requirements. Proper usage strategies, a comprehensive environmental management system (EMS), and a forward-thinking Emergency Response Plan will also remain vital tools for companies potentially dealing with PFAS to effectively manage the associated risks.

Environmental Justice (EJ)

The focus on EJ remains a top priority for the Biden Administration. In November 2023, EPA announced the largest single investment in EJ history, funded by President Biden’s Inflation Reduction Act. The Community Change Grants build on Biden’s Justice40 Initiative and will provide approximately $2 billion in funding for community-driven projects that deploy clean energy, strengthen climate resilience, and build capacity to manage environmental and climate justice challenges. EPA also launched the EJ Thriving Communities Grantmaking Program to expand its technical assistance and project grants for communities, as well as the EJScreen screening and mapping tool, which provides EPA with a consistent approach for combining environmental and demographic socioeconomic indicators.

Guidance: Take the time to understand the communities where you operate—be informed, be prepared, and be proactive. Establish organization priorities and goals and commit the appropriate resources to address EJ concerns. With EPA focused on more regulations, more enforcement, and improved climate change and EJ, environmental management needs to play an integral role in company strategy.

Chemical Safety

EPA is working to strengthen chemical safety with the long-awaited implementation of the 2016 amendments to the Toxic Substances Control Act (TSCA). In addition, the Agency has advanced rules to better protect communities from harmful chemicals like TCE and methylene chloride. These rulemakings align with Goal 7 of the FY 2022-2026 EPA Strategic Plan to ensure the safety of chemicals for people and the environment.

Guidance: Facilities need to have a good understanding of chemicals used onsite so they can take action now to phase out any regulated chemicals (e.g., TCE), as the phaseout period will be quick. Take an inventory of onsite chemicals to determine what chemicals the facility manufactures, distributes, and/or uses. For many chemicals, safer alternatives may be available to eliminate the use of banned chemicals. Be aware of compliance deadlines as you make the transition.

Other Issues to Watch

The following OSHA issues also ones to watch in 2024:

- OSHA Hazard Communications Standard (HCS): In 2021, OSHA proposed to modify the HCS to maintain conformity with the United Nations Globally Harmonized System (GHS) revision 7, align certain provisions with Canadian and other U.S. agencies, and address issues with the 2012 HCS. The proposed updates are intended to increase worker protections and reduce the incidence of chemical-related occupational illnesses and injuries by improving the information on labels and safety data sheets (SDS) for hazardous chemicals. The Agency expects to release finalized changes to the HCS in early 2024.

- OSHA Emergency Response Standard: OSHA has released an unofficial version of its new Emergency Response Proposed Rule and anticipates publication in the Federal Register in January 2024. The proposed rule would replace OSHA’s existing Fire Brigades Standard (29 CFR 1910.156), which covers only a subset of emergency responders. The proposed Rule provides basic workplace protection for workers who respond to emergencies as part of their regularly assigned duties (e.g., fire departments, emergency medical service, and technical search and rescue).

- OSHA National Emphasis Program (NEP) on Warehousing and Distribution Center Operations: Effective July 13, 2023, OSHA announced an NEP for inspections at warehousing and distribution centers, mail/postal processing and distribution centers, and other high-risk retail establishments. The comprehensive safety inspections will focus on workplace hazards common to those industries, including powered industrial vehicle operations, material handling/storage, walking-working surfaces, means of egress, and fire protection.

Set Your Goals for 2024

There is a common need across industry to manage emerging EHS risks with solutions that also provide transparency, security, and sustainability. Heightened EPA enforcement, new OSHA reporting requirements, and pending SEC requirements for ESG are necessitating solutions to help manage business and EHS requirements—and that will continue in 2024.

KTL suggests completing the following early in 2024:

- Get senior leadership commitment. Even with the best EHS personnel, the organization and its EHS system will only be as good as the top leadership and what is important to them.

- Conduct a comprehensive gap assessment to ensure you are meeting the requirements of all applicable EHS regulations, particularly given new environmental, health and safety, and ESG requirements. Think critically about what you have and how overlapping requirements may apply (e.g., your chemical inventory may uncover requirements for air permitting, waste management, Tier II report, etc.). This assessment should be the starting place for understanding your regulatory obligations and current compliance status.

- Seek third-party oversight. Having external experts periodically look inside your company provides an objective view of operations, helps you to prepare for audits, and allows you to implement corrective/preventive actions that ensure compliance. An outside expert can often provide the “big picture” view of what you have vs. what you need; how your plans, programs, and requirements intersect; and how you can best comply.

- Create an integrated management system (e.g., ISO 9001/14001/45001) by finding commonalities between the standards and leveraging pieces of each to develop a reliable system that works for your organization.

- Leverage IT solutions—whether to inventory chemicals and GHG emissions, track OSHA performance, or manage compliance requirements. Technology advancements can help create significant business efficiencies.

Comments: No Comments

EPA Regulatory Alert: Enhanced PFAS Reporting

Per- and polyfluoroalkyl substances (PFAS) are a group of manmade chemicals that have been manufactured and used in a variety of industries since the 1940s. PFAS are often referred to as “forever chemicals”. They are very persistent in the environment and the human body, where they bioaccumulate in blood and organs over time. Most PFAS exposure comes through ingesting food and water that becomes contaminated with PFAS when it migrates into soil, water, and air during use and/or disposal. Studies show that exposure to PFAS may be linked to harmful health effects in humans and animals.

The Environmental Protection Agency (EPA) has taken a number of actions to tackle PFAS contamination, including the development of a PFAS Strategic Roadmap to confront the human health and environmental risks of PFAS. In October 2023, the Agency finalized two new rules to improve reporting on PFAS.

TRI Reporting Requirements

The Toxic Release Inventory (TRI) tracks the management of certain toxic chemicals that may pose a threat to human health and the environment. U.S. facilities in different industry sectors must report annually how much of each chemical is released to the environment and/or managed through recycling, energy recovery, and treatment.

EPA’s new rule designates PFAS as chemicals of special concern for TRI reporting purposes and, correspondingly, eliminates the exemption that allowed facilities to avoid reporting information on PFAS when those chemicals were in small concentrations (i.e., under 100 pounds). However, PFAS are often used at low concentrations in many products. By removing this exemption, covered industry sectors and federal facilities that use any of the 189 TRI-listed PFAS will have to disclose any quantity of PFAS they manage or release into the environment.

By eliminating the de minimus exemption, EPA will receive more comprehensive data on PFAS, including quantities of chemicals released into the environment or managed as waste, to support more informed decision-making.

TSCA Reporting and Recordkeeping Requirements

EPA also published a final rule under the Toxic Substances Control Act (TSCA) that will require any entity that has manufactured or imported PFAS in any year since 2011 to report information on its uses, production volumes, disposal, exposures, and hazards.

Specifically, these facilities will have 18 months following the effective date of the rule to report the following data to EPA for each PFAS chemical substance or mixture:

- Covered common/trade name, chemical identity, and molecular structure.

- Category(ies) of use.

- Total amount manufactured or processed, amounts for each category of use, and estimates of the respective proposed amounts.

- Descriptions of byproducts resulting from manufacture, processing, use, or disposal.

- Information regarding environmental and health effects.

- Number of individuals exposed and reasonable estimates of the number of individuals who will be exposed in their workplace and the duration of exposure.

- Manner or method of disposal.

This rule is intended to help EPA better characterize the sources and quantities of manufactured PFAS in the U.S. by creating the largest-ever dataset of PFAS manufactured and used in the U.S.

How This Impacts You/What You Need to Do

Federal and state initiatives and regulations to manage PFAS are rapidly growing. KTL does not see the challenges associated with PFAS going away any time soon. If anything, we anticipate more facilities will be directly impacted by mitigation efforts and regulatory action to support EPA’s PFAS Strategic Roadmap, such as those outlined above.

It is important for facilities to have a good understanding of PFAS and PFAS-containing chemicals used onsite, as reporting requirements now apply regardless of the quantity used. Implementing a chemical inventory management system that documents and manages PFAS data can make reporting more efficient and help ensure the facility meets these new requirements. Proper usage strategies, a comprehensive environmental management system (EMS), and a forward-thinking Emergency Response Plan will also remain vital tools for companies potentially dealing with PFAS to effectively manage the associated risks.

Comments: No Comments

EPA Regulatory Alert: Ban on TCE

Trichloroethylene (TCE) is an extremely toxic chemical used in cleaning and furniture care products, degreasers, brake cleaners, and tire repair sealants, amongst other uses. TCE is commonly found at Superfund sites as a contaminant in soil and groundwater. It is known to cause liver cancer, kidney cancer, and non-Hodgkin’s lymphoma, as well as damage to the central nervous system, immune system, reproductive organs, and fetal health. Environmental and human health risks are present with even very small concentrations of TCE.

Proposed Rule

On October 23, 2023, EPA issued a proposed rule under the Toxic Substances Control Act (TSCA) to ban the manufacture, processing, distribution, and use of TCE to prevent soil and groundwater contamination and protect the public from the associated health risks. This proposal aligns with President Biden’s Cancer Moonshot approach to end cancer and advances the Administration’s commitment to environmental justice.

EPA’s proposed TCE ban would phase out the manufacturing, processing, distribution, and use of TCE over the course of one year. For uses where a longer transition timeframe is necessary (e.g., critical Federal Agency uses, battery separators, manufacture of certain refrigerants), EPA is proposing stringent worker protections to reduce exposure while phasing out TCE.

How This Impacts You/What You Need to Do

It is important for facilities to have a good understanding of chemicals used onsite and to start taking action now to phase out any TCE, as the one-year phaseout period will be quick. Facilities should:

- Inventory Chemicals: Take an inventory of onsite chemicals to determine whether the facility manufactures, distributes, and/or uses any TCE. Consult safety data sheets (SDS) for ingredients. TCE can be referred to as trichlor, trike, or tri and may be sold under a variety of trade names. TCE is identified by its Chemical Abstract Service (CAS) Number: 79-01-6.

- Identify Alternatives: For most uses of TCE as a solvent, safer alternatives are already available. EPA’s Safer Choice Program provides a list of solvents (including degreasers) identified as “safer” alternatives. The University of Massachusetts Toxics Use Reduction Institute (TURI) also has an extensive database of safer alternatives to TCE (and other toxic solvents and cleaners) used for degreasing purposes.

- Make the Transition: The best way to prevent TCE from entering the environment is to eliminate its use in facility operations (i.e., source reduction). Follow EPA’s Pollution Prevention (P2) approach to implement cleaning and degreasing modifications, such as switching to aqueous and less toxic cleaning solvents, adopting other mechanical cleaning techniques, or substituting equipment.

- Dispose Correctly: TCE waste can be characterized in a few ways depending on what it is and how it is used (or not used). TCE waste should be properly characterized and managed at a permitted disposal facility—most likely an incinerator.

Comments: No Comments

EPA Regulatory Alert: TSCA Risk Evaluation Process

The Environmental Protection Agency’s (EPA) Toxic Substances Control Act (TSCA) (modified in 2016 by the Frank R. Lautenberg Chemical Safety Act) requires EPA to conduct a risk evaluation to determine whether a chemical substance presents an unreasonable risk to health or the environment under the conditions of use.

On October 19, 2023, EPA proposed a new rule to strengthen its process for conducting these risk evaluations under TSCA. The rule is intended to:

- Ensure EPA’s processes better align with the provisions of the law.

- Support more robust evaluations that account for all risks.

- Provide a foundation for protecting workers and communities from toxic chemicals with more protective rules for workers and communities.

TSCA Background

The TSCA inventory is a list of all existing chemical substances manufactured, processed, or imported in the U.S. The current inventory contains 86,718 chemicals, of which 42,242 are active in U.S. commerce. EPA evaluates existing and new chemicals for the inventory:

- Existing chemicals: EPA prioritizes existing chemicals on the list and selects chemicals to determine if the risk is reasonable or unreasonable. If the risk is unreasonable, EPA will impose restrictions to eliminate the risk. The list of ongoing and completed evaluations is available online.

- New chemicals: Any chemical that is not currently on the inventory is considered a “new chemical substance.” Anyone who plans to manufacture or import a new chemical substance for a non-exempt commercial purpose must provide EPA with a Premanufacture Notice (PMN) at least 90 days before initiating the activity. During the notice review period, EPA will review the PMN and determine if the chemical presents unreasonable risk(s) to human health or the environment.

Proposed Provisions

The new proposed rule aims to strengthen EPA’s process for conducting its TSCA chemical risk evaluations. EPA initially finalized a risk evaluation framework rule in 2017; however, it was quickly challenged in Court. The October 2023 proposed rule addresses the Court’s revisions and adds provisions requiring that risk evaluations:

- Consider the disproportionate harms facing overburdened communities, including multiple exposure pathways to the same chemical and combined risks from multiple chemicals.

- Be comprehensive and not exclude conditions of use or exposure pathways.

- Consider risks to workers.

- Use best available science.

- Provide a single determination of whether the chemical presents unreasonable risk, rather than multiple determinations based on individual chemical uses.

- Ensure transparency through updated risk evaluation documents.

- Better align manufacturer-requested risk evaluations with EPA-initiated risk evaluations.

While many of these changes were announced in 2021 and have been incorporated into TSCA risk evaluations over the past two years, they have not been finalized in the Code of Federal Regulations. Doing so will help ensure more certainty regarding the process for conducting TSCA risk evaluations moving forward.

How This Impacts You/What You Need to Do

This rulemaking aligns with Goal 7 of the FY 2022-2026 EPA Strategic Plan to ensure the safety of chemicals for people and the environment. That Plan focuses on strengthening EPA’s ability to successfully implement TSCA with appropriate resources to complete EPA-initiated chemical risk evaluations and risk management actions.

- If you manufacture or import chemicals, determine if the chemical is on the TSCA inventory.

- If you manufacture or import a chemical that is not on the inventory, complete a PMN at least 90 days before initiating the activity.

EPA will conduct a risk evaluation to determine the risk(s) the chemical poses to human health or the environment. Under the proposed rule, these evaluations will be more robust to account for all risks to better protect workers and communities from toxic chemicals.

Comments: No Comments

Environmental Non-Conformances: Knowledge Is Power

Audits offer a systematic, objective tool to assess compliance across the workplace and to identify any opportunities for improvement. Audits can also present an opportunity for organizational learning and development, particularly related to non-conformances. In many cases, non-conformances are not a result of intentionally ignoring the requirements; rather, they can often be attributed to not fully understanding compliance requirements.

KTL has identified three areas where our environmental auditors repeatedly identify non-conformances that stem from lack of knowledge or understanding—and what companies need to know to eliminate them.

Waste Handling

Do you know your generator status? If a facility does not accurately determine its generator status, it will likely have waste handling non-conformances during an audit.

Generator status is determined by the volume of hazardous waste the facility generates per month and accumulates onsite. There are three categories of generators:

- Very Small Quantity Generator (VSQG)

- Small Quantity Generator (SQGs)

- Large Quantity Generator (LQG)

Determining which category a facility falls into is key to understanding which requirements apply and, subsequently, maintaining compliance. How much waste does the facility generate? How much waste does the facility accumulate? What types of risks does this waste present? This information will dictate whether the facility is a VSQG, SQG, or LQG.

Hazardous waste generator status should be registered with the Environmental Protection Agency (EPA) and/or state environmental agency. Generator status can be verified in the EPA’s Enforcement and Compliance History Online (ECHO) database. If the information is incorrect, the facility will need to complete Form 8700-12 to ensure generator status is correct, as VSQGs, SQGs, and LQGs have some different requirements due to their potential impacts on the environment. From there, the facility should identify the applicable regulatory requirements and train staff on their responsibilities to avoid non-conformances.

Chemical Spillage

Any facility that generates waste needs to determine what waste is hazardous. In the event of a spill, it is critical that the facility can characterize whether the spill cleanup is hazardous or nonhazardous, as that will dictate the appropriate response. If a waste determination/characterization has been completed, this can typically be determined from the chemical’s Safety Data Sheet (SDS).

Emergency preparedness is another element of compliance when it comes to a spill. Facilities need to make sure supplies are appropriate for any spill that could potentially occur. For example, if a forklift battery leaks, that is an acid spill. The facility spill kit should contain baking soda to neutralize the acid.

Universal Waste

EPA regulates a class of waste referred to as universal waste. Universal wastes are hazardous in their composition but can be recycled. Under EPA’s definition, the following are the current universal waste streams:

- Batteries (Li, Ni-Cd, Ag, Hg)

- Mercury-containing equipment (MCE)

- Electric lamps

- Cathode ray tubes (in electronics)

- Pesticides (recalled or farmer-generated)

- Non-empty aerosol cans (in some states)

- Others, as determined by state-specific regulations

EPA regulators have focused on these waste streams as a source of penalty for the past decade. Failure to collect, label, store, and recycle universal waste properly is one of the most frequent citations issued. Although not as complex as the requirements for proper hazardous waste management, universal waste has nuances that a generator must be aware of to properly meet the regulatory requirements.

Universal waste doesn’t “count” against generator status. It does not have to be manifested but generally requires specific labeling language (e.g., universal waste lamp, universal waste battery). Universal waste must also be stored in closed, intact containers. Universal waste can only be kept onsite for one year, so these containers should be dated when the first waste is added as a best practice or a log/schedule should be maintained of dates. A mail-back program for universal waste may be an appropriate consideration for generators of small quantities of universal waste to comply with disposal regulations.

Remedy for Compliance

Many of the non-conformances found in these three areas can be relatively simply remedied—or avoided altogether by making sure facilities educate and train impacted staff on how to:

- Inventory, characterize, and quantify wastes.

- Determine/verify generator status.

- Identify applicable federal and state regulatory requirements based on the above. States may have additional rules provided they are at least as stringent as the federal requirements.

- Implement the appropriate procedures, programs, systems, and training to eliminate non-conformances.